Join War on the Rocks and gain access to content trusted by policymakers, military leaders, and strategic thinkers worldwide.

Every year, the Congressional Budget Office (CBO) releases a long-term budget outlook, usually during the summer. But it might just as well be Groundhog Day.

In the 2011 outlook, noting poor long-term budget trends, the CBO’s analysts wrote on page 33:

A large amount of debt could also harm national security by constraining military spending in times of crisis or limiting the country’s ability to prepare for a crisis.

The same or similar passages appeared in 2012, 2013, 2014, 2015, and 2016. In the 2017 outlook, the most recent report, devotees of the warning could find it on page 6:

A large debt also can compromise a country’s national security by constraining military spending in times of international crisis or by limiting its ability to prepare for such a crisis.

The newly released Trump administration tax plan has reintroduced the issue of the U.S. federal deficit and debt. There will surely be a robust debate about current spending, taxation, and program priorities. But inevitably lost in this debate will be an issue that policymakers have avoided for years and appear intent to continue to avoid: the strongly negative long-term budget outlook. Bold promises and even actions that bring the budget into balance for the short term should not mask the fact that the U.S. government has failed to face its long-term budget problems.

Without changes, the already historically high national debt will continue to rise, and the government’s ability to pay for many functions — including defense — will rely wholly on borrowed money, calling into question the ability to sustain those functions.

This punting could have strongly negative consequences for U.S. security. Continued budget imbalances will crowd out discretionary spending, of which defense comprises about half. With decades-long procurement cycles, weapons-system development and acquisition is always uncertain. It will become more so in the future when money is far tighter, confronting U.S. security strategists with a decline in available resources but no corresponding decline in tasks desired by policymakers. Furthermore, as the veterans of the Iraq and Afghanistan wars grow older, the costs of their health care are likely to continue to rise, making further demands on the federal budget.

For Congress and the president, the steps are clear: Regardless of one’s policy preferences, matching revenues to spending is essential. If left unaddressed, continuing deficits and rising U.S. debt could lead the government to cut programs and services, and a rising tax burden could slow U.S. growth and therefore tax receipts, leading to further cuts.

And for defense policymakers, the path is also clear. Without fixing the long-term imbalance, it is unlikely that the increased spending levels proposed by the House and Senate Armed Services Committee chairs will be sustainable for more than a few years. Defense officials need to emphasize more strongly the importance of fixing the federal budget, and plan more aggressively for meeting national security goals in a constrained environment.

How We Got Here: Budget History and Projections

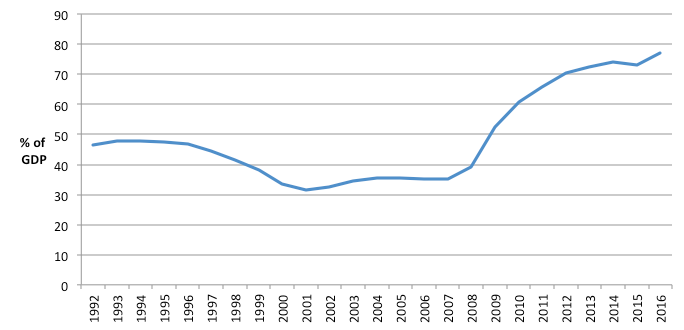

Since the end of World War II, from 1946 to 2016, the federal budget has been in deficit 60 times. But overall debt always remained under control, even as the rare surpluses of 1998 to 2001 evolved back to deficits (Figure 1). This gave the government leeway to borrow in times of emergency. Even by 2008, debt remained below 40 percent of GDP.

Figure 1. Federal Debt Held by the Public, 1992-2016, Percent of GDP

Source: Congressional Budget Office, An Update to the Budget and Economic Outlook: 2017 to 2027, June 2017.

This changed with the Great Recession. The U.S. budget system provides automatic fiscal stimulus during economic downturns, for example through such transfer payments as unemployment insurance and through decreases in tax revenues stemming from reduced incomes. The response to the Great Recession also included a discretionary fiscal stimulus, raising deficit spending further. Many economists argued this was necessary, and some retrospectives indicate that it helped save the United States from more dire economic outcomes.

But except for a slight decline relative to GDP in 2015, the federal debt kept rising faster than the economy. The slow recovery resulted in below-average revenues through 2014. Even after revenues started rising, spending remained even higher, staying above its long-term average through at least 2016. And as of now, these deficits and the debt increase have no end in sight.

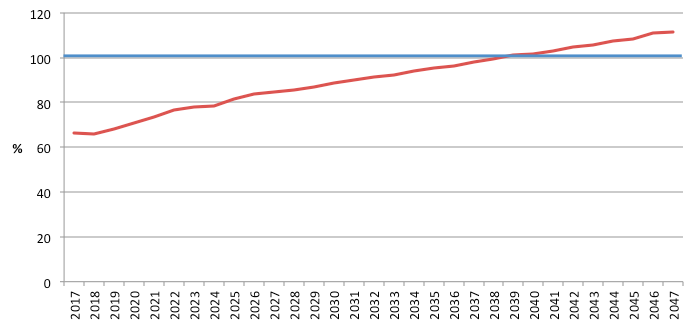

Ominously, current CBO projections suggest that federal spending on entitlements along with interest on the national debt will amount to 100 percent of federal revenues by 2039 (Figure 2). Interest rates will deliver a double hit. Thus far, historically low interest rates have accompanied the recent increase in debt. But interest rates will likely start rising, so even at the same level of debt, required federal payments will increase.

Put differently, after 2039 the federal government will need to borrow if it wants to spend so much as a penny on environmental protection, education, transportation, veterans’ benefits and services, administration of justice, diplomacy, and defense.

Figure 2. Entitlements and Interest as a Percent of Federal Revenues

Notes: “Entitlements” include Social Security, Medicare, Medicaid, CHIP, ACA Marketplace Subsidies, and Basic Health Program insurance. Source: Summary Extended Baseline in Supplemental data file for CBO, The 2017 Long-Term Budget Outlook, March 2017.

Budget Warnings and Inadequate Solutions

The CBO has been one among many voices warning about the long-term budget shortfall. The Government Accountability Office Comptroller General Gene Dodaro has raised this issue, as did his predecessor, David M. Walker. Outside the government, the Center for a Responsible Federal Budget has been raising alarms for years, trotting out an all-star cast of economic and budget experts. One former federal economic official now at Stanford University warned in 2011 that “the long term budget problem begins now.” For those reluctant to read boring government or policy reports, there’s even a snazzy GAO video, with live-action analysts.

And yet, Congress and successive presidential administrations have done little to address the problem.

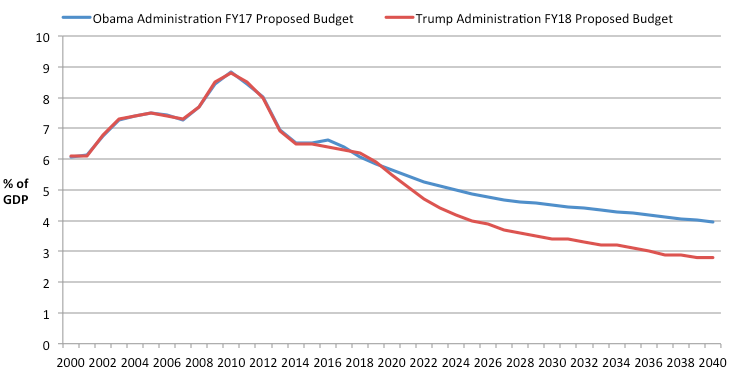

In its FY17 budget proposal, its last, the Obama administration proposed policies that over the long term would stabilize the federal debt held by the public at 78.3 percent of GDP in 2038, compared to 76.5 percent in 2016 — well below CBO’s most recent projection of 116 percent in 2038 under current policy. It’s possible that these proposals would have helped manage the debt, but the deficit and debt projections depended on assumptions about the economy and politics through 2040 that were unlikely to hold. The budget path had an element of paying Tuesday for a hamburger today — the plan projected deficit and debt increases as a percentage of GDP into the 2030s, leaving the implementation of fiscal tightening to future Congresses and presidents.

Not only that, the proposal projected a steady decline of discretionary spending — about half of which is defense — from 6.6 percent of GDP in 2016 to only 3.9 percent of GDP in 2040 (Figure 3).

Figure 3. The Projected Relative Decline in Federal Discretionary Spending

Sources: Office of Management and Budget, Budget of the U.S. Government, Fiscal Year 2017, February 2016: Long Range Budget Projections for the FY 2017 Budget; and Office of Management and Budget, Budget of the U.S. Government: A New Foundation for Greatness, Fiscal Year 2018, May 2017: Long Range Budget Projections for the FY 2018 Budget.

Moreover, even if the proposals had been viable, they weren’t as ambitious as they appeared: Except for 1944–1948 and 1950, the debt has never been as high as 78.3 percent.

The Trump administration’s FY18 budget proposal was far more aggressive on deficit and debt reduction over the long term. It proposed an immediate reduction in the federal debt held by the public in 2018, and then a steady decline to 29.2 percent of GDP by 2040. But as with the Obama budget, this also rested on assumptions that may turn out to be incorrect.

Like Obama’s budget, the new Trump plan projected that discretionary spending would fall, in this case to only 2.8 percent of GDP by 2040. This would be crushing pressure on discretionary spending relative to historical norms.

Defense spending alone was 3.1 percent of GDP in 2016. So even if the entire discretionary spending budget were handed to defense, under Trump’s plan resources would still be more constrained than they are now.

Fixing the Budget

The United States has been facing a potentially exploding deficit and rising debt for at least a decade.

But as demonstrated by the failure of the Budget Control Act of 2011 to have a noticeable effect on the national debt, efforts to date have been far from sufficient. Bringing the budget into balance is likely to continue to be difficult.

The policy solutions are well-known. Even with faster economic growth, spending cuts and tax increases will be needed. Potential measures include a carbon tax, which would not only raise revenue but take a precautionary step against climate change, a value added tax, or raising the retirement age for Social Security. And there will also likely need to be further adjustments to how the nation pays for health care.

This effort should include repairs to what has become a strange and extraordinarily complex tax system. Measures could involve cutting such popular benefits as the home mortgage interest deduction, and taxing employer-provided health insurance. There are numerous options for achieving budget balance and debt control. In recent years, the various credits, deductions, preferences, and benefits in the tax code have cost more than $1 trillion in lost revenue, almost as much as revenue from individual and corporate income taxes, or almost enough to bring the budget close to balance.

Issues for the Armed Forces

The Department of Defense has not yet experienced the kinds of hard choices that significant cuts in spending will force. Although the Budget Control Act raised the threat of dire consequences, it ultimately had only a modest effect on defense spending, because Congress found ways to scale back what were supposed to be large cuts. The Bipartisan Budget Act of 2013 raised defense spending caps by $32 billion over two years, and the Bipartisan Budget Act of 2015 raised the caps by another $40 billion over the next two years.

It is doubtful such stopgaps can continue for much longer. Thus, for the Department of Defense and U.S. armed forces, there are two steps that could be followed.

First, civilian and military defense officials can continue to make clear to Congress and the public that the military power underlying America’s security depends heavily on the health of the overall U.S. economy and the ability of the federal government to pay for that power. Part of this will necessarily involve explaining the threats that the United States faces and how the military contributes to U.S. security and prosperity. Officials can hardly lobby for specific tax increases or revenue cuts. But former Chairman of the Joint Chiefs of Staff Admiral Michael Mullen and others have forcefully made the case for a sustainable budget that can support appropriate defense spending. This should continue.

In some ways, defense spending differs from other forms of spending — appeals to patriotism or concerns about security threats can lead the public to support defense spending over spending on, for example, scientific research or the arts. On the other hand, defense spending is a larger target, and cuts to other programs are likely to be felt more personally. Already skeptical of the use of military force around the world, the taxpaying population will be unlikely to endure cuts to programs whose benefits are close to home without also calling for cuts in defense and other international spending.

Second, defense officials need to plan for a constrained environment. There needs to be more contingency planning for the downside — a budget environment with less money for personnel, equipment, training, and other tasks.

This planning is easier said than done. Even before future cuts, the defense budget does not rest on a sound base. In the 2014 Quadrennial Defense Review, General Martin Dempsey, then-Chairman of the Joint Chiefs of Staff, wrote that he expected security challenges, and with them demands on the armed forces, to increase:

In the next 10 years, I expect the risk of interstate conflict in East Asia to rise, the vulnerability of our platforms and basing to increase, our technology edge to erode, instability to persist in the Middle East, and threats by violent extremist organizations to endure.

And, he added, the readiness of U.S. forces, which had suffered “devastating impacts” from sequestration and budget cuts, “will worsen over the next 3 to 4 years.”

Other assessments of the deterrent balance in East Asia (such as that by David Ochmanek in 2015) and on NATO’s eastern flank (such as that by David A. Shlapak and Michael Johnson in 2016) have identified serious shortfalls in U.S. military posture and capabilities, raising concerns about the credibility of U.S. security guarantees. Absent substantial and sustained increases in spending on force modernization, these trends will worsen.

Where Does the United States Stand?

These problems do not necessarily foreshadow dire economic consequences, but they do cast doubt on America’s ability to maintain its role as the preeminent economic and military superpower.

The United States is not Mexico before its 1982 economic collapse. In 1976, Mexican scholar and diplomat Daniel Cosío Villegas remarked, “Have you seen the size of our external debt? … We are screwed.” Mexico held large amounts of debt denominated in dollars, so that as the value of its currency fell, the cost of its debt in local currency rose. In contrast, U.S. debt is denominated in dollars, so even if the value of the dollar changes relative to foreign currencies, the cost of paying back the debt will not change.

Japan has lived well enough with epic levels of public debt and is likely to continue to do so. But the United States is also not Japan. As the architect and guardian of the post-WWII international system that has provided unprecedented levels of prosperity and security, the United States took on a variety of costly obligations that, so far, have benefited not only the rest of the world, but America as well. Without a serious approach to the deficit and debt, the United States faces a future of slow economic growth, reduced military spending, growing challenges to its credibility as a security partner, and reduced international influence.

Nothing is certain, especially long-term projections. Also uncertain is which page of the budget outlook CBO will choose for its annual debt warning. But given past performance, we can be pretty certain it will be somewhere in the report for yet another year.

Howard J. Shatz is a senior economist at the nonpartisan, nonprofit RAND Corporation, where he focuses on international economics and economics and national security. He is the author of U.S. International Economic Strategy in a Turbulent World (RAND Corporation, 2016).

Image: U.S. Army/