Join War on the Rocks and gain access to content trusted by policymakers, military leaders, and strategic thinkers worldwide.

The U.S. military is not only the world’s most advanced force, but it is also the busiest and most widely deployed. The Defense Department’s constant commitments leave it caught in a metaphoric hamster wheel of activity, with important implications for its strategy and investment plans. Gallons of ink have been spilled debating defense spending priorities and force modernization. Now, we should spare a few drops to discuss the resulting trade-offs in force readiness and operating tempo as well as what this all means for military contractors.

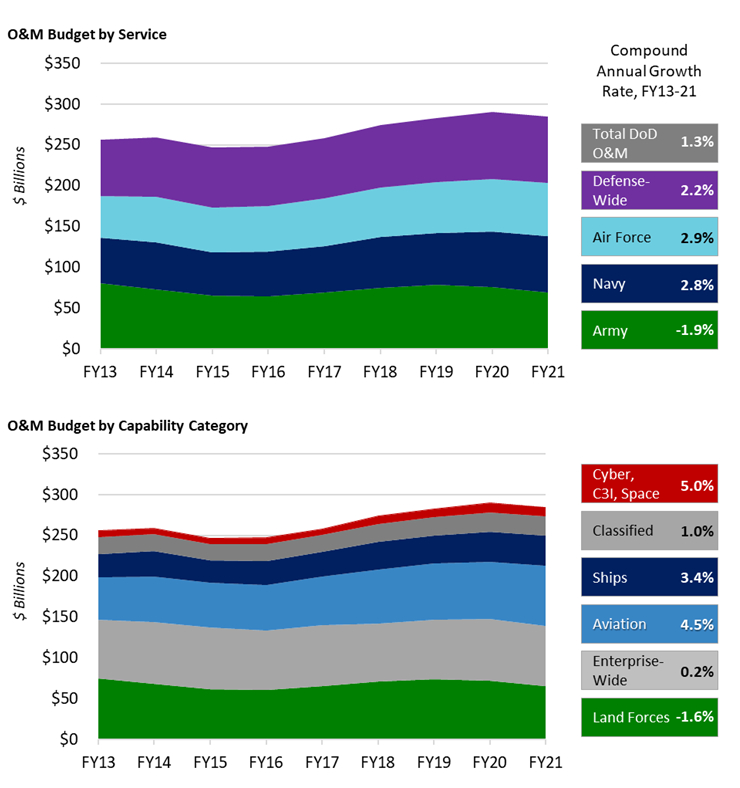

The Defense Department’s top-line budget is likely to remain fixed or even decline in the coming years. The military’s push for technological innovation will require money, and Congress will continue to fund military-linked manufacturing. This means that the Defense Department will need to find deep savings elsewhere, including in its Operations & Maintenance (O&M) budget. O&M pays for equipment and facilities maintenance, fuel, spare parts, and training services, making it the lifeblood of U.S. forces across all service and operating domains (see figure 1). The salaries and benefits for most Defense Department civilian employees are paid from O&M accounts. O&M is also a major source of funding for contractor personnel who support the Defense Department in areas like information technology, engineering, logistics, and administration. Since the 1970s, the O&M budget has tended to grow at a relentless, if gradual, pace when benchmarked against the size of U.S. military forces. In Fiscal Year 2020, the O&M budget accounted for about 42 percent of the defense budget.

As a result, cutting the O&M budget won’t be easy. There are three main areas where cuts could occur: reduced overhead, smaller force size, and lower readiness/slower operating tempo. Examining each of these areas suggests that readiness and operating tempo will be the most likely to yield savings. This, in turn, has important implications for where firms across the defense industry might see the biggest contractions in their contracts.

Figure 1: Operations & Maintenance Budget

Source: Avascent analysis of Defense Department O-1 budget documents

Where to Cut?

Reduced Overhead

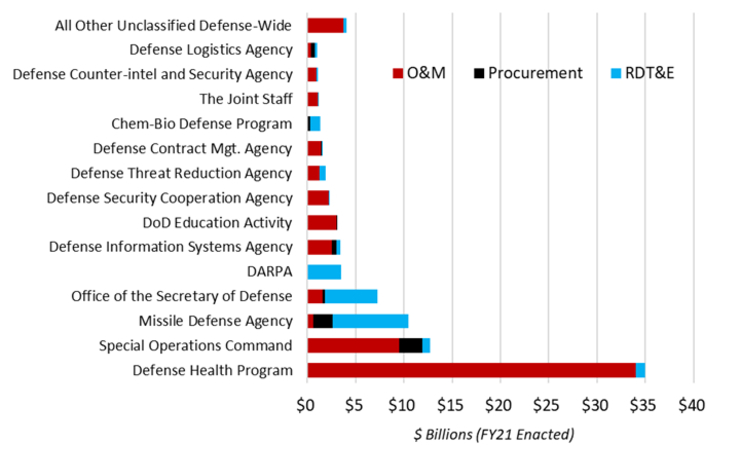

The Defense Department should not plan on using savings from reduced overhead to offset the costs of its innovation agenda. The Defense Department has attempted to reduce overhead costs for years, which means there is little low-hanging fruit left to pluck. During the Donald Trump administration, then Secretary of Defense Mark Esper pushed hard to cut costs among the so-called Fourth Estate — that is, the defense agencies that primarily serve administrative and management functions (see figure 2). But it remains unclear whether these efforts yielded substantial results. What’s more, eliminating any of these agencies will be hard to do since most of them serve functions that are essential to the department’s operations. Some of these agencies are critical to modernization efforts (the Defense Advanced Research Projects Agency, the Missile Defense Agency) or operating capabilities (Special Operations Command, the Defense Information Systems Agency). Other agencies, such as the Department of Defense Education Activity and the Defense Health Agency, sustain the Department of Defense as an institution. Many of these enjoy strong support because of the services they provide to uniformed personnel and their families.

Figure 2: The Fourth Estate (Operations & Maintenance and Other Major Budget Accounts)

Source: Avascent analysis of Defense Department budget accounts. Chart does not include classified funding attributed to defense-wide accounts. Chart excludes chemical agent & munitions destruction.

Smaller Force Size or Changed Force Mix

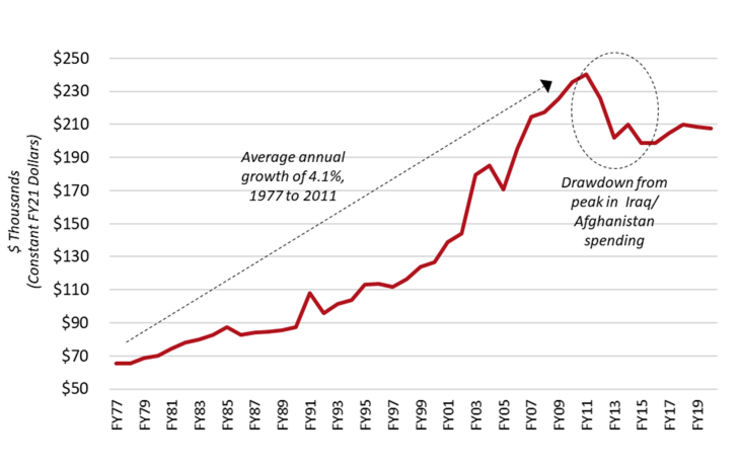

The size of U.S. military forces tends to be a major driver of O&M costs. Whether measured in “end strength” (uniformed personnel) or in force structure (number of operational units), bigger is more expensive. Indeed, even a force that does not change in size over time will tend to consume more and more O&M funding as inflation affects the vast array of goods and services required to sustain it. Since the late 1970s, the O&M cost per active servicemember has increased at a relentless pace (see figure 3).

Figure 3: Operations & Maintenance Budget per Active Servicemember

Source: Avascent analysis of Defense Department budget documents

Each of the armed services is likely to grow or shrink in different ways during the coming period. It has become a widely held view in Washington that the Army may have no choice but to yield savings for higher priority space, aviation, naval, and cyber forces. A defense strategy that emphasizes the Indo-Pacific theater and confronts an increasingly capable Chinese military will put less importance on some Army forces. When she was with the Center for Strategic and International Studies in 2020, Deputy Defense Secretary Kathleen Hicks authored a report that suggested the Army might need to absorb “a sizeable reduction.” For their part, Army leaders can be expected to fight this view tooth and nail.

The Air Force, by contrast, is unlikely to dramatically grow or shrink in size. Given its central role in the vast Indo-Pacific theater, substantial reductions are out of the question. Yet, the Air Force’s ambition to grow from 312 to 386 operational squadrons, articulated in 2018, may also have fallen by the wayside. Spinning out various units to constitute the Space Force has obviated parts of that plan. The new Air Force chief of staff, Gen. Charles Q. Brown, has suggested that modernizing the force will be a bigger priority than growing its size. Having the Air Force transition to a much more “unmanned” force could theoretically reduce the service’s operating costs. But while the proliferation of remotely operated aircraft has vastly increased the Defense Department’s capacity to perform both strike operations and intelligence, surveillance, and reconnaissance missions, it has not lowered the operating cost of U.S. forces. While these systems may not have pilots in the cockpit, they still require substantial involvement of military and civilian personnel as well as other supporting costs.

The Navy, like the Air Force, aims to expand its forces in response to increasing demands. While the Navy has articulated varying objectives for its fleet size in recent years, these plans have always envisioned more than the 297 battle force ships in the fleet today. But whether the Navy builds toward a fleet of 297 ships, 355 ships, or 500 ships, the cost to own and operate that fleet will continue to rise. Figure 4 shows that the Navy is already spending more O&M dollars to sustain a steady or declining level of operational tempo.

Figure 4: Navy Operations & Maintenance Budget by Capability Category and Ship Operational Tempo

Source: Operations & Maintenance figures from Avascent analysis of Defense Department O-1 documents. Operational tempo figures are from Defense Department FY2021 operations & maintenance overview. Operational tempo figures measure the number of days per quarter ships were underway on their own power. Operational tempo figures shown here are for the active U.S. Navy only. Operations & maintenance budget counts total Navy.

There have been serious proposals to migrate toward a different force mix with greater emphasis on smaller surface combatants and unmanned surface and undersea vessels. Advocates for these concepts argue they offer superior operational capability at a more sustainable cost. But quick progress down this path is unlikely. There has been disagreement among the Navy, Congress, and the Office of the Secretary of Defense on a range of issues linked to fleet transformation. The expansion of Chinese military power has increased the urgency of these issues. But that urgency has not yielded a consensus on a path forward.

Lower Readiness and/or Slower Operating Tempo

Rather than reduce the size of the force that it sustains, the Department of Defense may contemplate reducing the money it spends to sustain that force on a day-to-day basis. Following this path would involve slowing the operating tempo and/or reducing the readiness of various units to undertake missions at a moment’s notice. In contrast to cutting the size of the force, which yields savings only in the long term, reducing readiness or operating tempo can yield substantial savings quickly. Purchases of fuel, spare parts, support equipment, and other supplies can be scaled back right away. The need for support services like training, maintenance, and logistics work can be reduced. Similarly, slowing down the flow of aircraft, ships, or vehicles through required depot maintenance cycles can yield substantial savings in the near term.

Of course, shifting to a lower level of operational tempo or readiness can come with a range of risks. Lower operational tempo reduces the availability of key assets, like carrier strike groups or fifth-generation fighter squadrons, relative to the demands of commanders looking to deter the nation’s adversaries. Compromises in readiness and O&M funding can also have consequences for the safety of military personnel and the civilians around them. The crashes of the Navy destroyers USS McCain and USS Fitzgerald in the Indo-Pacific in 2017 illustrate the risks of reducing staffing, training, and maintenance over an extended period of time.

However, some Department of Defense leaders may be ready to explore changes in readiness and operational tempo. In February, Air Force Chief of Staff Gen. Charles Q. Brown and Marine Corps Commandant Gen. David H. Berger argued that “a fixation on ‘readiness,’ and how it is conceptualized,” has prevented the Department of Defense from pursuing its critical investment priorities. The two service chiefs also explained that the Department of Defense should change how it measures readiness, accounting for future operating capabilities and not just near-term force availability.

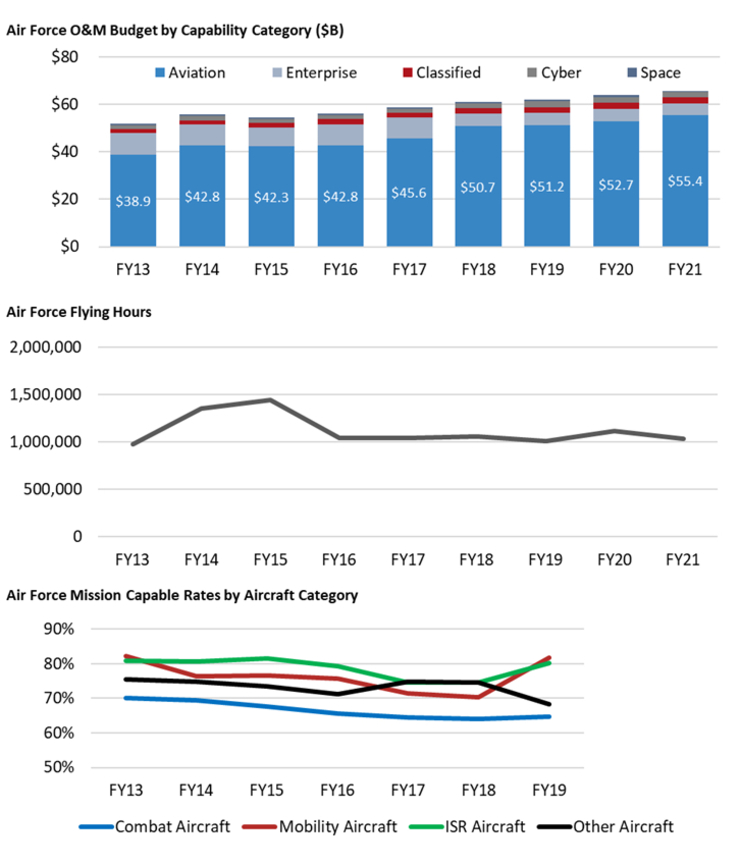

The Air Force’s recent spending on operational tempo and readiness offers a hint as to why this may be an area of change. Air Force advocates often observe that the Air Force is both the “smallest and oldest” that it has ever been in terms of the size of its aircraft inventory and the average age of its jets. The data show that it has also never been more expensive to operate and sustain. Despite a significant increase in aircraft-related O&M spending, the Air Force has seen flat to declining flying hours and aircraft mission capable rates, particularly among its combat aircraft (see figure 5). This explains why Brown is eager to throttle back on the service’s O&M costs. What is less clear is how this would impact the Air Force’s ability to meet near-term global demands.

Figure 5: Air Force Operations & Maintenance, Flying Hours, and Mission Capable Rates

Source: Operations & maintenance figures from Avascent analysis of Defense Department O-1 documents. Flying hours from Defense Department operations & maintenance overview. Mission capable rates from Air Force Times, Air Force Magazine, and Military Times. Mission capable rates average figures for all relevant inventories. Figures cover the active Air Force, Air Force Reserve, and Air National Guard.

The Army may also be reconsidering how it measures readiness, with possible implications for O&M costs. Gen. Michael Garret, chief of U.S. Army Forces Command, has indicated that the Army may institute a new Regionally Aligned Readiness and Modernization Model, which aims to better balance periods of relatively high operational tempo with “down” periods in which Army units can focus on training and modernization. Building intervals into the rotational system during which Army personnel can recuperate from deployments and units can induct new equipment might create some O&M savings, even if this is not the goal of the new model.

The Navy may have less inclination to pursue financial savings in its readiness accounts. The service has been working to correct a series of maintenance, training, and other shortfalls that began in the wake of the 2013 budget sequester. In addition to the 2017 crashes, the 2020 fire that destroyed the USS Bonhomme Richard while in port in San Diego has been blamed, in part, on shortfalls in training and other readiness measures. Increasing the size of the fleet while also working to improve readiness will preclude reductions in the Navy’s O&M budget. While an increased reliance on smaller as well as robotic warships might eventually reduce the O&M cost per hull, this will take many years to dramatically change the composition of the force.

Reducing readiness and/or operational tempo will remain extremely difficult so long as U.S. combatant commanders rely on these forces for military operations around the world. Early in his tenure, Secretary of Defense Lloyd Austin launched a Global Force Posture Review intended to assess “how we best allocate military forces in pursuit of national interests.” This has the potential to rationalize the demand for military forces with supply and potentially relieve pressure on O&M costs. But drawing back on forward-deployed military forces will be particularly challenging at a time when the Biden administration aims to demonstrate U.S. resolve to China and Russia and reopen negotiations with Iran from a position of strength.

Implications for Contractors

What would O&M cuts mean for those who supply the products and services that the Defense Department purchases with them?

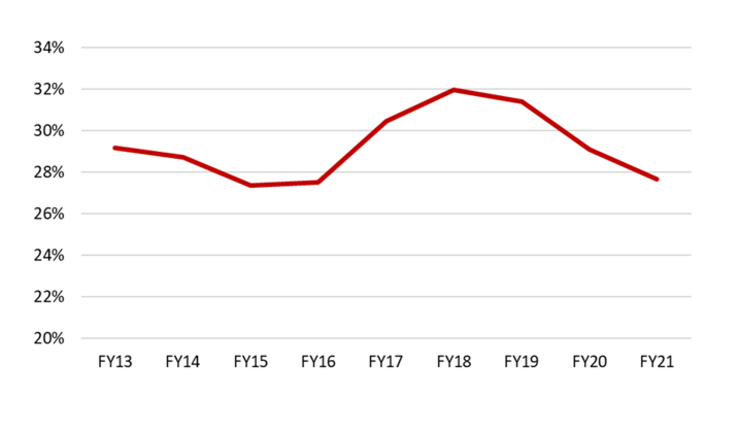

O&M accounts are used to acquire a nearly infinite array of goods and services. Defense Department figures suggest that an average of almost 30 percent of the O&M budget is contracted out, including advisory and assistance services, equipment sustainment, health care, and facilities upkeep (see figure 6). Another 15 percent of the O&M budget goes toward purchasing equipment, supplies, and spare parts. As a result, cuts in the O&M budget will have major implications across the defense industry.

Figure 6: Contract Services as a Share of Operations & Maintenance Budget

Source: Defense Department operations & maintenance overview

Personnel

A broad belt-tightening, particularly among headquarters and administrative organizations, could squeeze both opportunity and margins for firms providing staff augmentation and other support services to these communities. Firms whose revenue is tied in some way to Army headcount or specific types of operational units would also be at risk. Not all Army forces will be affected by the coming downturn in the same way, however. Organizations, personnel, and facilities related to, say, air and missile defense may remain less affected than other Army forces.

Training

Many goods and services related to live training could come in for reductions if the Defense Department pursues reductions in force size, readiness, or operational tempo. Air Force flying hours seem likely to decline, for example. But live training is just one form of training. Virtual and constructive training, drawing on various forms of simulation, seem likely to increase in importance. This may have implications for training services, software products, simulation systems, and training infrastructure integration.

Maintenance and Sustainment Engineering

As with training, the impact of cuts in maintenance and related engineering services will vary across the military. If the Air Force does look to economize on the number of hours some aircraft are flown each year, this will come with a commensurate decline in their demand for spare parts and maintenance. But we don’t yet know whether the Army, Marine Corps, and Navy will follow suit or whether the Air Force will treat all aircraft equally. Fifth-generation aircraft like the F-35, F-22, and B-2 are particularly costly to sustain, but other cheaper aircraft could see more sustained operational tempo and maintenance requirements.

Logistics Support

Each year, the Department of Defense spends billions on contractor support for a diverse array of logistical and related technical services. These contracts can vary widely in scope, geographic span, and structure. In some areas, a decline in the number of uniformed military personnel may actually increase the need for contractor support. Services that are connected to parts of the force that contract in size or scale back in readiness will obviously see greater risk. If the Biden administration looks to reduce the U.S. forward presence in the Middle East or elsewhere, some reduction in demand for associated logistical support would follow.

Facilities Sustainment

One of the Defense Department’s biggest costs is maintaining a sprawling infrastructure of bases and facilities. In FY2018, this amounted to 585,000 buildings located on 4,775 sites around the world. With the level of polarization in Congress and the very narrow margin of control by Democrats in both the Senate and the House, it is unlikely that the Biden administration will push hard for a new round of base realignment and closures, even if defense leaders believe there is excess capacity. But the department may have other means of economizing on its network of facilities short of formal closures. This would mean a marginal reduction in demand for maintenance and operation of physical plants, which is often performed by small businesses.

Looking Ahead

Two realities will shape the Defense Department in the coming years. First is the centrality of China’s rising power in defense planning. Second is a stagnant or declining top-line defense budget. Finding a way to sustain or even accelerate the pace of modernization and innovation in the Defense Department will necessitate cutting the O&M budget. Given the hard choices this entails, it will be essential for the armed services and defense agencies — as well as their contractors — to find ways to support U.S. military forces at a lower cost.

Doug Berenson is a managing director at Avascent, a global consulting firm serving clients in government-driven markets like defense, aerospace, and cyber. Doug has been with the firm for 20 years, helping government and corporate clients forecast trends in demand, weigh investment options, and make effective policy decisions.

Image: U.S. Air Force (Photo by Staff Sgt. Trevor T. McBride)

{kind=link}