Join War on the Rocks and gain access to content trusted by policymakers, military leaders, and strategic thinkers worldwide.

Ronald Reagan: “I am not worried about the deficit. It is big enough to take care of itself.” Increased the national debt by $1.86 trillion (186 percent)

George H.W. Bush: “Read my lips: no new taxes.” Increased the national debt by $1.554 trillion (54 percent)

Bill Clinton: “You mean to tell me that the success of my program and my reelection hinges on the Federal Reserve and a bunch of f*cking bond traders?” Increased the national debt by $1.396 trillion (32 percent)

George W. Bush: “Once we have funded our national security and our homeland security, the final great priority of my budget is economic security for the American people. To achieve these great national objectives — to win the war, protect the homeland, and revitalize our economy — our budget will run a deficit that will be small and short-term, so long as Congress restrains spending and acts in a fiscally responsible manner.” Increased the national debt by $5.849 trillion (101 percent)

Barack Obama: “Today I’m pledging to cut the deficit we inherited by half by the end of my first term in office…I refuse to leave our children with a debt that they cannot repay, and that means taking responsibility right now, in this administration, for getting our spending under control.” Increased the national debt by $8.588 trillion (74 percent)

Donald Trump: “I’m the king of debt. I love debt.” TBD.

When President Donald Trump signed the Bipartisan Budget Act of 2018 on Feb. 9, ending the second brief government shutdown of the year, a nearly decade-long era of fiscal austerity came to a definitive end. The legislation increased discretionary spending by almost $300 billion over two years, a decisive break from previous years’ spending deals where appropriations grew at or just above inflation. Many in the aerospace and defense sector celebrated the signing of the bill, with growing expectations of good times to come. But it is essential to understand how long these boom times might last. Austerity politics will return again to dominate the budget scene, as they always do. Austerity politics, or deficit politics, refers to legislating either reduced spending or limited spending growth with the aim of reducing the deficit – the gap between revenue and outlays. Deficit politics have reared their head in almost every past presidential administration. It is unlikely this time will be different and the defense industry should plan accordingly.

Even before Trump signed the bill, most industry observers had expected that with unified control of Congress, Republicans would be more willing to countenance increased deficits. The previous period of unified Republican control – from 2003 until 2007 under President George W. Bush – saw significantly higher deficits. However, after passing tax cuts that increased the deficit by an estimated $1-1.5 trillion over ten years and a major disaster-relief bill without offsets, it remained to be seen whether the GOP’s patience for deficits would extend to a deal on discretionary spending. In February, the Bipartisan Budget Act offered a definitive answer by adding hundreds of billions of dollars to discretionary spending in fiscal years 2018 and 2019 with almost no offsets, significantly increasing the deficit. Spending will undoubtedly increase further in 2020 and 2021, with defense hawks and Democrats viewing the new spending levels as a baseline rather than a short-term uptick. After dominating debates over government spending for much of the last decade, austerity politics and its advocates have been routed for the immediate future. But history suggests that beyond the next few years, their influence may return.

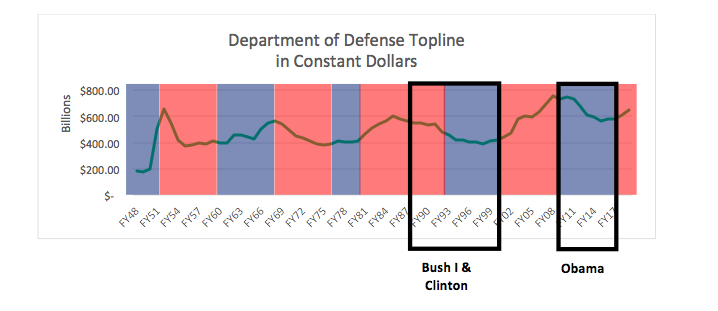

Defense Spending is Cyclical: A Short History

(Figures from OMB Historical Tables)

Defense spending has a long and established history of boom and bust, with the general trend towards increasing in real value over time. To understand the recent transition from a climate of austerity to one of rising government spending – and the likely coming reversal of that trend – the last two periods of retrenchment and expansion are instructive.

President George H.W. Bush entered office in 1989 facing rising deficits, the result of expanded domestic spending, tax cuts, and limited economic growth in the latter half of the 1980s. In addition, interest rates and borrowing costs, after trending down for most of the Reagan years, shot up in 1988 and remained high through the beginning of the Bush administration. The result was austerity politics: Bush sought to reduce deficits through the Omnibus Budget Reconciliation Act of 1990,which infamously violated his “read my lips, no new taxes” pledge by raising taxes on higher earners and reducing discretionary and mandatory spending. Following the passage of this legislation, real defense spending declined steadily (with a slight uptick in FY 1991 in response to the Gulf War) through FY 1994.

During the Clinton administration, defense spending continued its downward trend. After a spike in interest rates in 1993, the Clinton administration was forced to focus on deficit reduction in the FY 1994 budget. This funding bill also contained significant deficit reduction. Defense spending continued to drift down until FY 1999, when it began to increase in response to overseas demands and eased fiscal pressures. From FY 1998 until FY 2001, the government ran a surplus, allowing spending on both defense and non-defense to rise.

By the time George W. Bush came to office, Department of Defense spending had inched back up to over $441 billion in today’s dollars. However, after 9/11 and the invasion of Iraq, defense spending rapidly increased. The last year of Bush administration budgeting (FY 2009) saw Pentagon spending at over $670 billion. This surge continued into the Obama administration, with overall defense spending peaking at just short of $690 billion in FY 2010. However, in the background, trends in the legislative budget process were getting worse as filibusters of appropriations bills became more common, leading to more continuing resolutions and creating problems with passing funding legislation. In spite of record low borrowing costs and historically low interest rates, voters and politicians in both parties were deeply concerned about deficits in FY 2008 and FY 2009, which both exceeded $1 trillion dollars.

After the 2010 midterm elections, deficit reduction became a driving force in Washington out of a combination of recession anxiety and political opportunism. Voters in 2010 had expressed a deep concern about the size of the deficit as well as the slowly recovering economy. Republicans pushed heavily to rein in the deficit during the 2010 campaign. At the same time, the Obama White House’s determination to draw down American forces overseas began to reduce defense spending levels. This put in place the forces that would drive significant reductions in defense spending over the next few years.

Following their historic victory, the Tea Party and a newly elected Republican House majority almost caused a default on the national debt to force through deficit reduction legislation. The Budget Control Act of 2011 first reduced spending by $917 billion, but also authorized a bipartisan, deficit reduction “super committee” to find over a trillion dollars in deficit reduction over the next ten years. The committee completely failed. The committee’s failure, in turn, triggered the sequestration caps on discretionary spending. If fully implemented, the caps would have severely cut defense spending from its FY 2012 levels. More importantly, defense and non-defense spending became inextricably linked through the imposition of the caps and the normalization of the filibuster. This dependency exacerbated an already poorly functioning legislative process, resulting in government shutdowns and major delays in passing appropriations. Even so, spending growth immediately stagnated, as the government lurched from two-year cap fix to two-year cap fix until the past year, when, following Trump’s election, Republicans returned to complete control of Congress and the White House.

Both historical peaks in defense spending were followed by efforts to retrench to reducing the deficit. Prior to the first Bush administration, defense spending had reached a high point. The deficit as a percentage of GDP peaked during the Reagan administration. Real defense spending grew fairly steadily from FY 1999 until FY 2008, at which point it stagnated for several years before the Budget Control Act of 2011 initiated a period of decline. Now spending is again on the upswing, but it remains to be seen how long this will last.

A Rosy Near-Term Spending Forecast

During the early days of the Trump administration, it was unclear how interested the new president would be in increasing defense spending. While Trump did request an additional $30 billion in funding for FY 2017, his eventual FY 2018 budget would have only seen a minor increase (2 percent) in year-over-year spending. This may have stemmed from attempts by Office of Management and Budget Director and known fiscal hawk Mick Mulvaney to balance the budget within ten years. Whatever the reason, the budget suggested that defense spending might not go up despite Trump’s rhetoric on the campaign trail.

However, Congress had other ideas. After years of deadlock between budget hawks, deficit hawks, and defense hawks that limited overall spending increases, the Bipartisan Budget Act of 2018 created a major increase in defense spending in FY 2018, followed by another significant increase in spending in the following fiscal year. Cumulative spending for the Department of Defense will increase by almost $90 billion from FY 2017 to FY 2019.

| FY 2017 | FY 2018 | FY 2019 | |

| Department of Defense Discretionary Spending | $606 | $663 | $686 |

However, the president’s FY 2019 budget request would appear to dampen hopes for this growth to continue. The rate of growth forecast in the Future Years Defense Plan, the five-year spending forecast provided by the Department of Defense as part of its budget request, is set at the rate of inflation for the next three years (roughly 2.3 percent year over year), an effort to keep down the long-term deficit impact of the president’s budget request. This would seem to indicate that this period of rapid growth will not be sustained.

That said, there are two reasons to suspect spending will increase at a higher rate than foreseen by the White House. First, congressional defense hawks and the Pentagon will almost certainly demand increased spending in FY 2020, as they did for 2018 and 2019. To do otherwise would require savings to be found by pulling back from current operations. While confusion continues to surround the president’s desire to remove troops from Syria, it is likely that the coming years will not see a major retrenchment from overseas commitments.

Moreover, all three military services face growing recapitalization costs over the next decade. The Air Force appears to have gotten per-plane costs on the F-35 under control, but plans to increase orders means near-term spending will continue to rise. However, the B-21 bomber is still in development, when cost increases are most likely to occur. At the same time, the Air Force is going to be attempting to recapitalize the nation’s nuclear arsenal, which will also likely cost more than expected.

The Navy is looking at major spending challenges as it pushes to increase the fleet size and replace the Ohio-class submarine. This means shipbuilding spending will have to exceed the Navy’s historical average by over 50 percent (over $21 billion per year instead of $14 billion per year). The Marine Corps also faces several major acquisition programs, particularly around the CH-53K and the Amphibious Combat Vehicle .

The Army does not face the same immediate wave of modernization in the mid-2020s, but towards the end of the next decade hard decisions will need to be made about recapitalization of rotorcraft and a new generation of ground vehicles. When you combine the likely demands of sustained operations with the modernization requirements ramping up, it is difficult to see spending growing at only the rate of inflation.

Second, since the Budget Control Act caps will remain in effect through FY 2021, another bipartisan deal will be required to avert sequestration. While it is difficult to forecast how the 2018 midterm congressional elections are going to go, it seems highly likely that both parties will be required to pass a funding deal, giving defense hawks and Democrats more leverage to push for increased discretionary spending. Given how many Republicans voted for the FY 2018 omnibus (H.R. 1625), the first appropriation bill passed under the caps set in the Balanced Budget Act, it appears the deficit hawks don’t have the numbers to derail any compromise between Democratic and Republican leadership. This sets the stage for increased spending in FY 2020 and FY 2021.

The Coming Crunch and What’s at Risk

While the near-term defense spending picture is bright, the coming years are likely to see higher pressure on government spending from a variety of fairly predictable sources. Yet the speed with which that pressure builds may catch politicians and executives off guard.

First, interest rates have begun rising and will likely continue to rise for the next several years, which pressures spending by making it more expensive for the government to both sell new debt and to service existing debt. Second, the population will continue to age, driving up federal spending on entitlements, particularly health care. Third, the tax overhaul that was passed last year will not pay for itself. The legislation is expected to reduce revenue by an estimated $1.5 trillion over the next ten years.

Currently, interest on the federal debt is fairly low, amounting to $263 billion in FY 2017. However, should rates rise as predicted by the Congressional Budget Office, borrowing costs will balloon to $965 billion by FY 2028. At the same time, spending on entitlements is likely to increase further. Projected spending on Medicare, Medicaid, and Social Security will account for over 60 percent of spending growth over the next 10 years, adding trillions in federal spending. The FY 2019 deficit is likely to be over $1 trillion dollars and these headwinds make it unlikely that the figure will be lower in any of the next few years. This will increase the national debt and, in turn, drive up the cost of borrowing, putting additional pressure on federal spending. At some point, the political response to running so far in the red will involve forcing defense to pay at least part of the bill, as was the case in the early 1990s and the years following the Budget Control Act of 2011.

In addition to these pressures, outside groups, actors within the administration, and members of Congress will likely continue to advocate for deficit reduction programs. Already we see a push in the House of Representatives to pass a constitutional amendment to balance the budget. Similarly, the White House and Mulvaney in particular are pushing to rescind some of the non-defense spending included in the Balanced Budget Act. While neither of these efforts is likely to result in successful legislation, they do point to the continued influence of deficit hawks.

At some point, Congress will be called upon to address these ballooning costs. The crucial question is when that will happen. It would be nice to think there was some sort of historical or mechanical relationship between rising interest rates and government decisions about spending, or rising deficits and spending, or, really, almost any deficit-related factor and spending. However, there does not seem to be any obvious correlation. Instead, deficit reduction ends up being a political decision, driven by politicians, bureaucrats, and the public.

The past two periods of deficit reduction have seen a Democrat in the White House, with congressional leadership of both parties involved. The last Republican president to attempt to enact legislation to deal with the federal deficit was George H.W. Bush in 1990. He subsequently received a primary challenge –in part for his decision to raise taxes as part of deficit reduction legislation – and, eventually, lost after only one term. This may have set a precedent that raising revenue, even in service of deficit reduction, would result in political difficulties. Both the next Republican president (his son, George W. Bush) and the current occupant of the White House have appeared deeply reluctant to consider any attempts to raise revenue. Even so, history shows that, when borrowing costs start to rise and deficits continue to swell, there can be intense political pressure on a president, however reluctant he or she may be, to rein in spending.

Defense policymakers and industry leaders should approach this period of increased spending with a clear understanding that it is unlikely to be sustained. The Department of Defense should move slowly on initiating major new programs, with the understanding that efforts to ramp funding three or four years down the line may be thwarted by stagnant toplines and intense competition for dollars. Meanwhile, industry leaders should think through where to invest to take advantage of near-term opportunities, recognizing that it may be difficult for the department to execute planned spending growth. Outside stakeholders should work to make sure that, as spending growth slows, the department is working to limit unnecessary spending and prioritize programs that address strategic demands. Austerity politics will return, and it’s important for decisionmakers to be prepared.

Matt Vallone is the Director of Research & Analysis at Avascent Analytics, where he leads a team of defense and space-focused analysts in producing research products and data analysis. Prior to working at Avascent, he worked as the Legislative Director for Congresswoman Carol Shea-Porter in the House of Representatives. He holds a Master’s in Security Policy Studies from the Elliott School at George Washington University and a Master’s in Business Administration from the Whittemore School of Business and Economics at the University of New Hampshire.

Image: The White House photo by Stephanie Chasez, Public domain, via Wikimedia Commons

.jpg){kind=link}