Join War on the Rocks and gain access to content trusted by policymakers, military leaders, and strategic thinkers worldwide.

The ongoing competition between the People’s Republic of China and the United States in the Pacific is at a low simmer. Despite public friction over the U.S. Navy’s freedom of navigation operations, Chinese island construction in the South China Sea, and massive Chinese cyberespionage, relations between United States and China are not particularly adversarial. The United States has a vested interest in the status quo, a position that some Chinese writers view as an unfair and unrealistic constraint on Chinese ambition. Yet relations have not degenerated into the kind of brinkmanship typical of U.S.–Soviet relations in the 1980s, or even U.S.–Russian relations today. The robust trade relationship between the United States and China dwarfs the limited trade between the United States and the Soviet Union, leading many analysts to conclude that open conflict today is unrealistic because of a presumed equal economic impact on both sides. A cursory analysis reveals that the reality is entirely different: Sino–American economic ties are asymmetrically interdependent rather than mutually dependent. This would strongly favor the United States in any conflict.

Even within the Department of Defense, there are occasional traces of the opinion that the economic ties between the two nations would effectively prevent any open war. Under this assumption, the interdependence of the two nations acts as a barrier to escalation. This position is not new. British parliamentarian Richard Cobden wrote extensively about economic coercion and the obsolescence of British military might, starting some 30 years before the Civil War broke out in the United States. In 1909, Sir Norman Angell published the Great Illusion, arguing that European economic interdependence effectively rendered militarism obsolete. Five years later, the tinderbox that was early 20th-century Europe exploded into the most devastating war in over 250 years. Even when the Great War ground to a halt, it set the stage for a worse one only 21 years later. The willingness to slug it out with economic partners was not limited to Europe, either. In the Pacific, the United States was Japan’s largest trading partner in 1940 when Japan signed the Tripartite Pact with Germany and Italy. In 1940 the trade volume between the United States and Japan had been on a steady increase throughout the Great Depression despite the U.S. embargo on scrap metal. In fact, Japan set itself on a course for war with virtually all of its major trading partners, more or less simultaneously.

Clearly, there are some credible doubts about the very idea that economic interdependence will prevent big wars. In many cases, warfare erupts between countries sharing borders over which trade routinely flows in peacetime. As world trade relationships have become increasingly globalized, the possibility exists that conflict could erupt with significant disruptive effects beyond the proximate combatants — similar to the effects observed from the Tanker War in the Persian Gulf. But we should not bank on the idea that trade interdependence will forestall conflict. The emergence of an effective global trade network may ensure that while markets may be disrupted, they can be rapidly reconstituted.

With respect to Sino–American trade, the economic effects of open warfare are heavily biased against China. For the exchange of goods, China’s top trade partners are the United States, Japan, Hong Kong, South Korea, and Germany, respectively. This places China in the center of a trade network that is dominated by countries which maintain a formal defense alliance with the United States. With the exception of Hong Kong, China’s top trade partners have a formal defense treaty with the United States. In fact, countries that have a bilateral (Japan, Korea) or multilateral (ANZUS, NATO) defense agreement with the United States account for over 44 percent of Chinese exports and are a source for over 45 percent of the country’s imports. In contrast, the top five partners for the United States (goods only) are Canada, China, Mexico, Japan, and Germany, with China accounting for 9 percent of our imports and 22 percent of our exports. That is a major trade imbalance, even before allied nations are taken into account. In 2014, the United States imported over $467 billion worth of goods from China while exporting $124 billion.

The goods exchanged are likewise not symmetrical. The main products that the United States receives from China are computers, broadcasting equipment, phones, office machine parts and furniture, while exporting soybeans, aircraft, automobiles, integrated circuits, and raw cotton. Viewed in total, China gets raw materials and the products of advanced, and complex manufacturing, while the United States gets consumer goods. The United States imports consumer goods that are assembled in China from parts not manufactured there — as the supply chain analysis for the iPhone reveals.

The United States thus has the upper hand in a cessation of trade goods, but also in terms of economic geography. Because of the extremely limited capacity of its cross-border links, China is effectively an island nation, and is hemmed in by unfavorable maritime terrain that the United States can exploit. The United States has also been described as an island nation by strategic theorists, but of its four coasts, two are entirely out of China’s reach, leaving only the Pacific and Alaskan coasts subject to China’s very limited power projection capability. Operating in the Eastern Pacific, outside their air defense and missile umbrella, would be extremely challenging for China in the face of overwhelming U.S. air and maritime superiority. Conversely, because of the maritime chokepoints stretching from the Straits of Malacca to Japan, China’s maritime trade can be interdicted by an offshore control or strategic interdiction campaign from well outside the ability of the People’s Liberation Army Navy (PLAN) to credibly project power.

In the event of actual hostilities, commercial interests will do much of the interdiction work for the United States. Maritime insurance policies do not typically cover either ship hulls or cargos in a war zone and additional riders must be purchased at substantial cost, if available at all. Besides Chinese-flagged vessels, commercial carriers might be unwilling to travel to Chinese ports at all, particularly if the United States conducts a modern offensive mining campaign. In such a case, the flow of raw materials, particularly energy, to China (particularly energy) could come to a shuddering halt, while the United States suffers a much more limited effect. China is dependent on ocean movement for over 96 percent of its foreign trade, with no viable overland alternatives. A maritime interdiction effort would interrupt the majority of China’s international trade from the majority of trading partners and cut 90 percent of total petroleum imports, leaving China with an unprecedented oil crisis and a shortfall of more than half of the country’s total oil consumption.

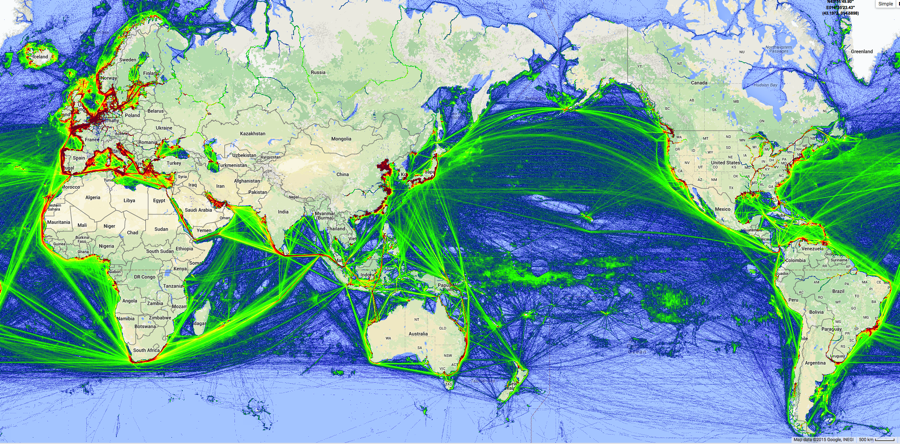

Worldwide maritime traffic density, all ships, 2014 (Marinetraffic.com)

The impact of a Pacific conflict would not just be limited to China. There could be a significant effect on the Japanese and Korean economies, even if they are not co-belligerents. China accounts for a quarter of Korea’s exports and a sixth of its imports (mostly electronics), making any collateral trade disruption significant, but not crippling. For Japan, the Chinese market accounts for about a fifth of both imports and exports. Neither Japan nor Korea is dependent on China for raw materials with one exception each: China supplies 40 percent of Korea’s steel imports and 59% of Japan’s rare earths.

Nevertheless, while Japan and Korea would suffer from a loss of trade with China, they are not in the same position whereby outside trade is easily interdicted. If a conflict erupted, maritime traffic which would normally pass through the Straits of Malacca will have to take the long way around, possibly doubling voyage time to avoid the waters adjoining the Chinese coast; but those trade routes need not pass through Chinese waters. Trade from the Americas need not deviate at all. Korea is more exposed to Chinese countermaritime efforts than Japan, given that some ports in both countries face China. However, the majority of South Korea’s port facilities border the Sea of Japan and not the Yellow Sea, which is shared with China and potentially very dangerous sailing. Japan’s ports largely face east and an interdiction effort by China would prove challenging. Again, the effect of a maritime threat is asymmetrical because both Korea and Japan have ready access to “friendly” waters while China does not.

The United States is not similarly constrained. The Pacific coast is not geographically hemmed in and the nearest island owned by an Asian country is Ostrov Mednyy, some 2500 nautical miles from Neah Bay, Washington. If the PRC could somehow force the closure of all 29 West Coast ports, it would affect barely a quarter of international trade. While significant, periodic labor disruptions have demonstrated that an effective West Coast port shutdown is not an economic catastrophe for the United States. From an energy standpoint, West Coast ports import about 40 million barrels of fuels and crude oil per month, barely 14 percent of the total U.S. import demand and 7 percent of the actual domestic consumption.

Chinese ports are comparatively far more vulnerable. Of the top ten container ports in the world, seven are Chinese. Los Angeles and Long Beach rank 19th and 21st with New York at 27th. Chinese ports are also transshipment centers, meaning that a large volume of traffic stops there and is then loaded on another ship headed to another destination. This makes Chinese ports vulnerable (from a business standpoint) to interdiction in a way that West Coast ports are not. It is likely that shipping trends will realign rather than transit through a war zone and this realignment may have lasting consequences. Normally, market forces drive a slow shift in transportation patterns, while a crisis could drive rapid changes. In early 2015, as the West Coast port dispute between the Pacific Maritime Association and the union continued, Vancouver saw a 15-percent jump in traffic in a month as the shipping market realigned away from U.S. ports.

There are other implications of any conflict with China, and it would be foolish to assume that a conflict could stay limited to the economic domain. The Chinese, for example, may well attack mainland U.S. infrastructure. Any open conflict with China is likely to be long and painful. But there is a built-in asymmetry with respect to the strategic positions held by the two nations. China is the disadvantaged partner in terms of trade volumes, maritime geography, alliance structures, and the makeup of goods exchanged. The impact of a conflict on international trade is likely to show a wide disparity, as the advantages of a North American location come into play. In any case, a conflict between the two powers will be expensive and will have severe collateral effects on global trade and trade patterns, but there is no historical evidence that would suggest that Sino–American trade relationships serve as a barrier to war. With any trans-Pacific trade disruption, the impact will be far more heavily felt by China.

Col. Mike “Starbaby” Pietrucha was an instructor electronic warfare officer in the F-4G Wild Weasel and the F-15E Strike Eagle, amassing 156 combat missions and taking part in 2.5 SAM kills over 10 combat deployments. As an irregular warfare operations officer, Col. Pietrucha has two additional combat deployments in the company of U.S. Army infantry, combat engineer, and military police units in Iraq and Afghanistan. The views expressed are those of the author and do not necessarily reflect the official policy or position of the Department of the Air Force or the U.S. Government.

Photo credit: OlliL